As we begin the second half of the year, I wanted to share a mid-year market update with our current perspectives. This includes the key themes shaping markets and what they mean for your portfolio.

Markets Were Strong in the First Half of the Year

The first half of 2026 was a reminder of why staying invested and maintaining a long-term perspective matters. Markets climbed to new all-time highs, corporate earnings grew at a double-digit pace, and a wide range of asset classes delivered strong returns. This all occurred even as the war in Iran, rising energy prices, and uncertainty around the Federal Reserve created short-term turbulence along the way.

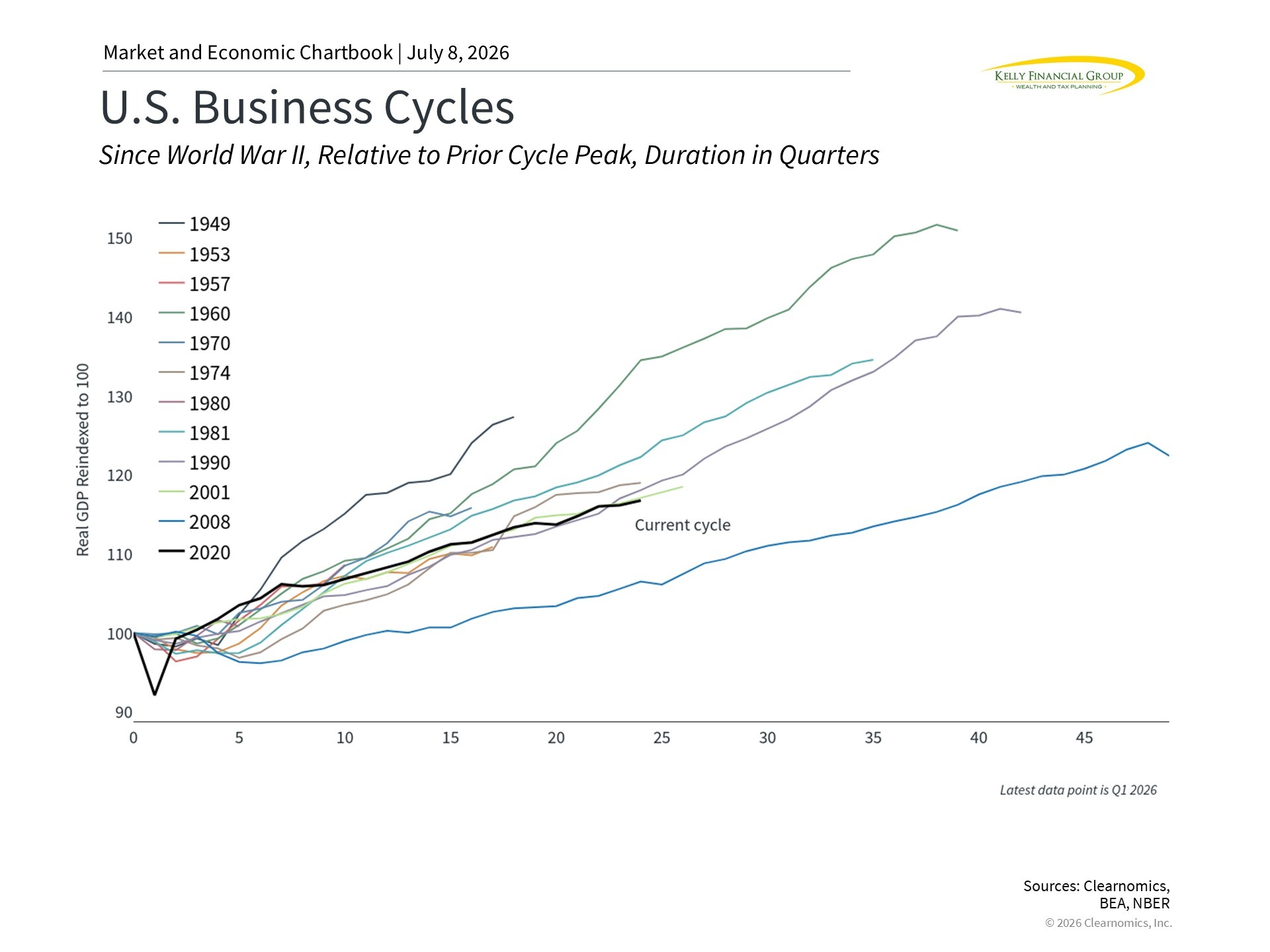

Perhaps the most important context is that the current business cycle is now in its seventh year and is going strong. There have been several moments in recent years when a recession seemed possible, including when inflation peaked in 2022 and when tariffs disrupted trade last year. However, the economy has been resilient throughout these periods and continues to grow.

Today, the economic picture remains broadly positive. The job market has strengthened this year, with payroll growth now averaging 111,000 jobs per month, above the long-term average. Consumer spending has also held up, business investment has accelerated due to AI trends, and the dollar has stabilized.

One potential challenge is that inflation remains elevated, largely because of higher energy prices. While the peace deal framework and ceasefire with Iran have been tentative, oil prices have still declined back toward their pre-conflict levels. This suggests that inflation may be near its high point for this cycle, although there are no guarantees on how this develops.

Steady economic growth has supported the stock market, with the S&P 500 reaching 24 new all-time highs so far this year. The S&P 500 returned 9.6% in the first half, while the Nasdaq gained 12.8% and the Dow Jones Industrial Average rose 8.9%. The second quarter was particularly strong, with the S&P 500 returning 14.9%. This was due to the timing of the market rebound, which began at the end of March.

Perhaps just as important is the breadth of performance across global asset classes. Emerging market stocks gained 22.7%, small-cap equities rose nearly as much, and commodities climbed 12.3%, driven largely by a strong first quarter. This kind of broad participation is one of the most encouraging developments for balanced portfolios and continues a positive trend that began last year.

What’s driving this? One major reason is that corporate earnings have supported returns, growing more than 20% over the past twelve months for S&P 500 companies. It is worth noting that U.S. stock valuations are elevated, with the S&P 500 trading at roughly 20 times forward earnings, above the long-term average of 16 times. High valuations do not predict what markets will do in the near term, but they are an important consideration.

For bond holdings, the current yield environment is among the most attractive in recent decades. The Bloomberg U.S. Aggregate Bond Index yields approximately 4.7%, well above its average of 3.0% since 2009. Investment-grade corporate bonds yield 5.1%. Bonds act as a source of income and a stabilizing force in a balanced portfolio.

Looking Ahead to the Second Half

There will no doubt be more periods of market volatility ahead. The war in Iran is ongoing, investors will continue to scrutinize the Fed, and the November midterm elections will attract attention in the media.

On that note, while it can be difficult to do, it’s important to keep our political views and financial goals separate. Markets have historically been positive under every combination of political party control. While headlines out of Washington D.C. may create short-term swings, the true drivers of markets are corporate earnings, economic fundamentals, and the business cycle.

Artificial intelligence continues to be a major theme across markets as well. Large technology companies are investing heavily in AI infrastructure, and high-profile IPOs including OpenAI and Anthropic are anticipated later this year.

Overall, this reflects market optimism. The key lesson from prior technology cycles is to take a longer-term view. During periods of rapid innovation, it can be difficult to identify the long-term winners in advance. The largest technology stocks today have taken decades to grow into the companies they are today.

The bottom line? The first half of 2026 has rewarded investors who remained diversified and focused on the long term, even as geopolitical and economic headlines created short-term uncertainty. As we navigate the second half of the year, it’s important to remember that your portfolio is designed for exactly this kind of environment.

As always, please do not hesitate to reach out if you have any questions or would simply like to discuss what any of these developments mean for your specific situation and goals.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.