I wanted to share some perspectives on current developments driving markets and what they mean for your portfolio, since there are many moving parts.

Overall, the stock market has performed well, reaching new all-time highs, with strong corporate profitability and a generally healthy economy. That said, there have also been recent swings in technology stocks, headlines on high-profile IPOs, and worries around rising inflation.

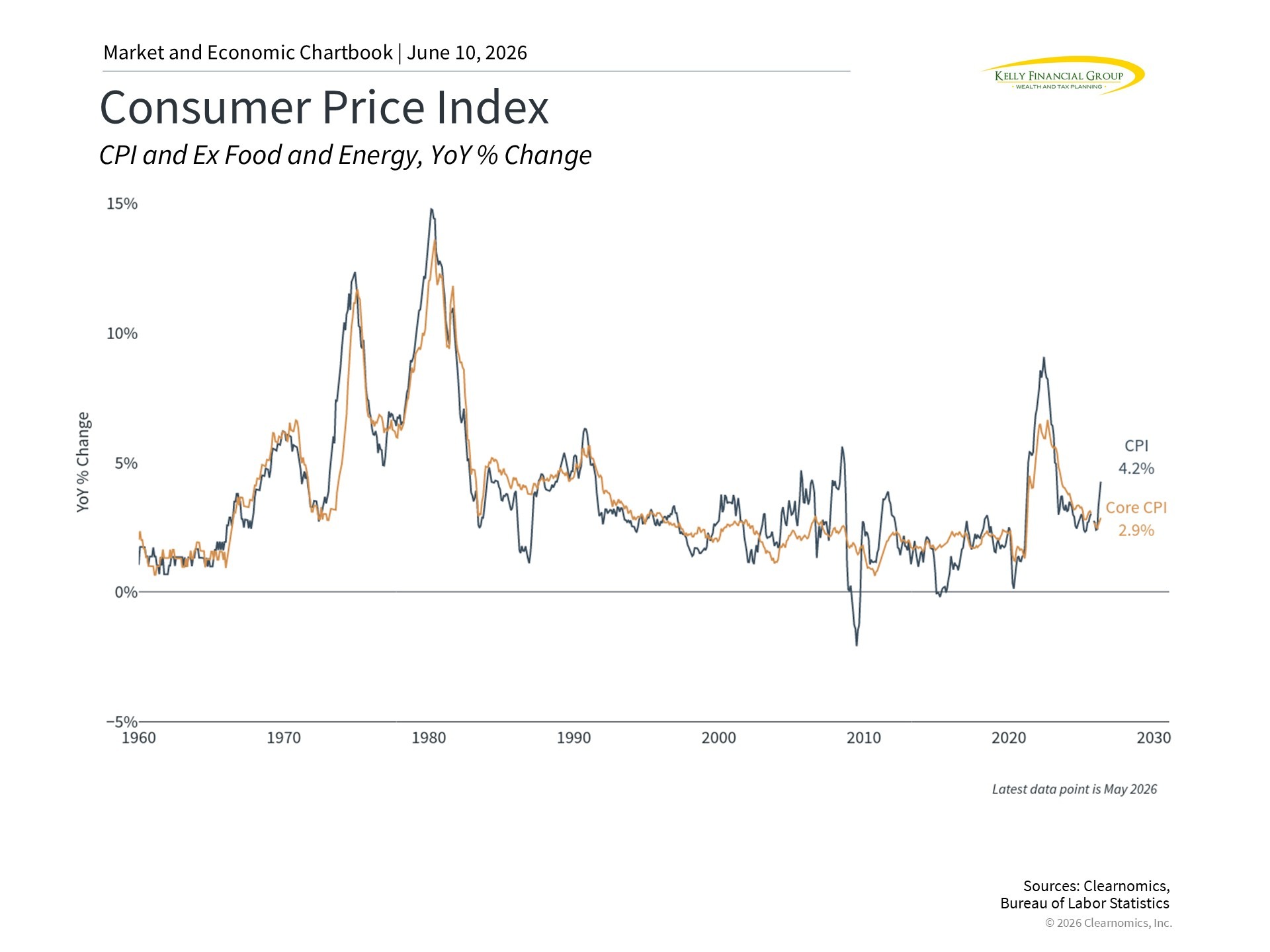

Much of the recent market swings come down to uncertainty around the Federal Reserve. After a strong jobs report and the Consumer Price Index rising at its fastest pace in three years, investors have begun to wonder whether the Fed might raise interest rates again. This shift in expectations is why technology stocks have become more volatile after a strong period.

Much of the rise in inflation is due to higher energy prices resulting from the war in Iran, and different inflation measures confirm this. For example, headline CPI rose 4.2% year-over-year, but when energy is excluded, CPI is only 2.9%. When excluding food, energy, and shelter, prices rose just 2.4%. In other words, while gasoline above $4 per gallon is a genuine challenge for households, these pressures have not yet spread broadly to other parts of the economy.

Why does any of this affect technology stocks in particular? Investors buy these companies largely because they expect high growth that extends far into the future, in contrast to more established businesses with steady cash flows. Since interest rates affect how those future profits are valued today, even small shifts, especially ones that change direction, can lead to larger swings.

A clear example of this sensitivity is the Magnificent 7, the group of large technology companies including Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla. From their peak at the end of 2021 to their bottom in late 2022, when inflation was heating up and rates jumped, this group lost about half of its value. They then recovered as rates stabilized and the Fed eventually started to cut rates, eventually rallying to new highs.

At the same time, the strong market environment means there is enthusiasm around initial public offerings, or IPOs. This includes a wave of large IPOs, particularly among companies related to artificial intelligence. A number of high-profile names, including SpaceX, Anthropic, and OpenAI, are in the process of going public after years in which relatively few companies did so.

IPOs are a positive market development since they make shares of these businesses available to a broader set of investors. However, it’s important to understand that IPOs are not just about how these stocks perform over the first few days. Instead, the largest tech companies today rose over decades from their IPOs.

For long-term investors, the encouraging news is that broad market indices automatically incorporate successful new companies as they grow. This means you gain exposure to successful IPOs over time without needing to invest in any single offering directly. It is important to keep in mind that many of these companies have grown for years through venture capital and private investment. By the time they go public, institutional investors and company insiders have often already participated in much of the early growth. Company insiders are also typically subject to lock-up periods during which they cannot sell their shares.

It is also worth remembering that IPO activity tends to come in waves, often during strong economic periods when capital is plentiful and enthusiasm is high. The late 1990s is the most famous example, and the post-pandemic surge in special purpose acquisition companies was a more recent one. Both were relatively short-lived, which is a reminder of why a longer-term perspective is important.

Bringing this back to your portfolio, a few points are worth emphasizing. First, expectations for Fed policy can change quickly. Even if current expectations prove correct, the Fed is not anticipated to raise rates until late in the year, and only by 0.25%. This is a modest move by historical standards, especially compared to the cycle from 2022 to 2023, when the Fed raised rates from near zero to 5.25% over 11 hikes.

Second, the stock market is coming off a strong period. While market swings are normal, and sometimes healthy, history shows that the stock market has performed well across many different rate environments, including periods when rates are rising, particularly when the economy is healthy enough to support corporate earnings.

Third, while recent volatility reflects shifting expectations around inflation and the Fed, and the excitement around IPOs is understandable, neither is a reason to fundamentally change your long-term plan. Your portfolio is designed to navigate exactly these kinds of environments.

As always, please do not hesitate to reach out if you have any questions, or if you would simply like to talk through what any of these developments mean for your specific situation and goals.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.