It has been a positive year so far for investors, so I wanted to share thoughts on the Federal Reserve and how it affects markets. The goal is to help you understand the role of the Fed, where monetary policy may go from here, and the impact on your portfolio.

The new head of the Fed, Kevin Warsh, was recently sworn into office. He replaces Jerome Powell, who will remain on the Fed’s Board of Governors. Leadership changes at the Fed naturally attract attention, partly because they don’t happen often, so it’s important to understand what this does and does not mean for the economy, markets, and portfolios.

History shows that these transitions rarely alter the long-term drivers of financial markets. What matters most for investors is understanding the environment the new Fed Chair is inheriting, what Warsh’s views suggest about future policy, and why the long-term investing principles that guide your financial plan remain as relevant as ever.

The Economy Has Grown Under Many Fed Leaders

To put this moment in perspective, it helps to zoom out. The Fed has had several chairs over the past 50 years, each facing a unique set of challenges. Paul Volcker battled the stagflation of the 1970s and early 1980s. Alan Greenspan navigated the dot-com boom and bust. Ben Bernanke implemented emergency policies during the 2008 global financial crisis. Janet Yellen oversaw the post-crisis recovery, and Jerome Powell managed the pandemic and the significant inflation surge that followed.

It is worth noting that while the Fed is often viewed as controlling the economy, the reality is that it is often reacting to events. Factors like technological change, demographics, energy prices, and global trade all shape the economy in ways that are beyond the Fed's direct influence. Its primary tools, including setting short-term interest rates and managing its balance sheet, also operate with what economists describe as “long and variable lags.”

Through all of these Fed leadership transitions, the U.S. economy has grown steadily. For investors, this is a reminder that while the Fed matters, it is just one of many forces at work.

Who Is Kevin Warsh?

Warsh is not new to the Fed. He served on the Fed's Board of Governors from 2006 to 2011, and was a decision-maker during the 2008 financial crisis. He developed a reputation as an inflation hawk, meaning he prefers keeping rates at levels that prevent inflation from worsening. Markets generally responded favorably to his nomination, viewing him as an experienced policymaker, especially in this environment of high fuel prices.

In his Senate confirmation testimony and recent writings, Warsh emphasized that monetary policy independence is essential. Warsh is often referred to as a reformer, but this does not necessarily mean he will seek to fundamentally change the Fed. After all, he fully supported the emergency stimulus measures during the financial crisis. Instead, for example, he has discussed narrowing the Fed’s focus and modifying how it communicates with the public.

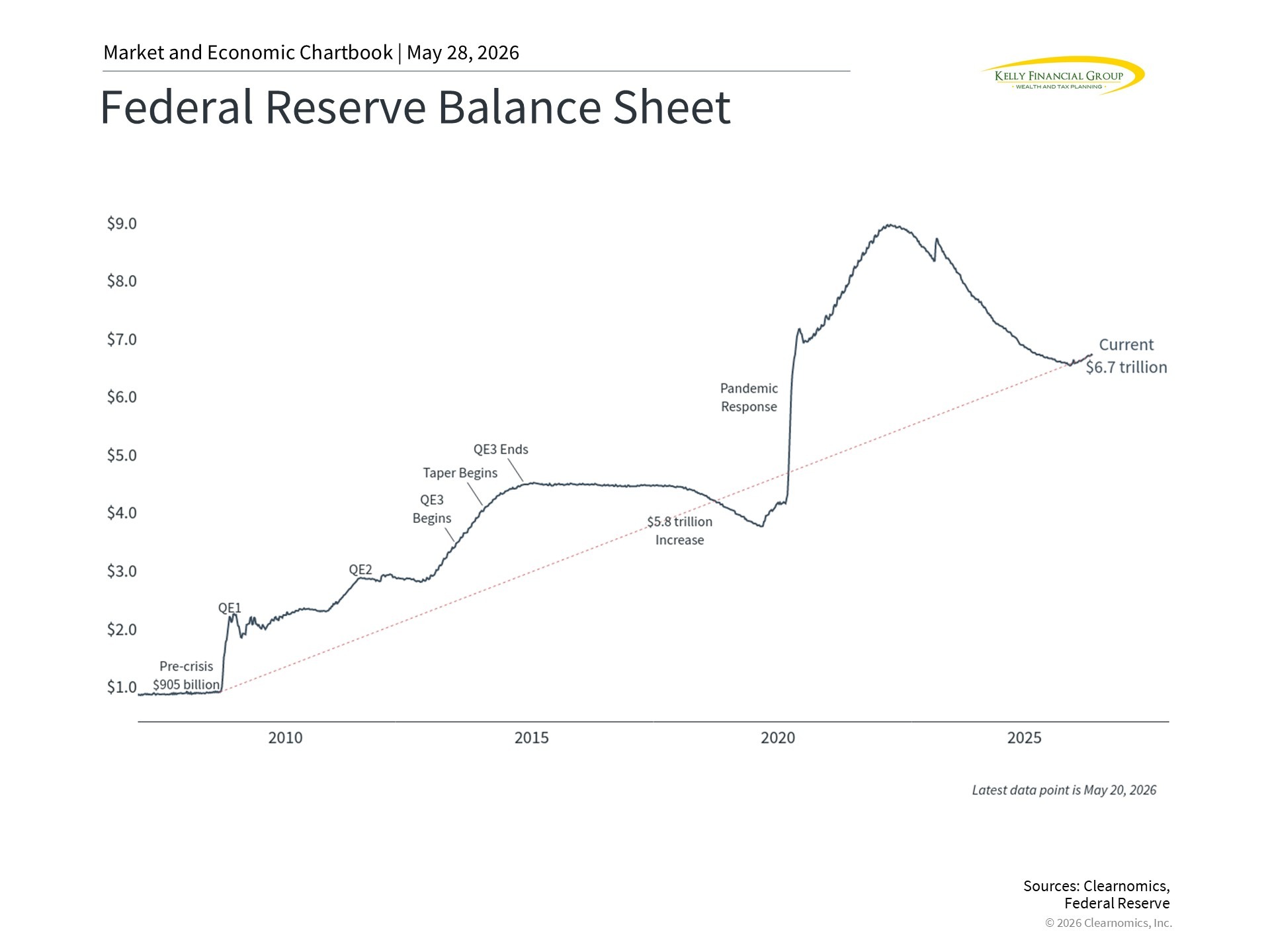

He has also expressed the view that the Fed's balance sheet, which remains large at approximately $6.7 trillion, should be reduced further. The balance sheet expands when the Fed buys bonds to support the financial system, a tool that has been used during crisis periods since 2008. Warsh believes that this ought to be symmetric, so that the Fed should reduce its balance sheet when these crises are over.

Fed officials have long tenures by design, meaning that the central bank often governs by consensus. It is important to note that how any Fed Chair actually governs is shaped by the economic conditions they face, the data available to them, and the input of the full Federal Open Market Committee (FOMC).

What This Means for Your Portfolio

Warsh comes into office during a mixed economic period which could affect monetary policy. On the one hand, inflation has picked up in recent months, driven largely by higher energy prices. On the other hand, the labor market has been weak over the past year, although it has improved in recent months. There has also been tension between the Fed and the White House over the level of interest rates.

This creates a difficult balancing act for the Fed, which can influence portfolio outcomes. Earlier this year, many investors expected the Fed to cut rates further. Now, market-based measures suggest the Fed could hike rates by early next year. Of course, these expectations can change quickly as the situation evolves.

For investors, an important implication is that the Fed may not cut rates again in the near future. Against this backdrop, bond yields have remained elevated this year. In fact, the 30-year U.S. Treasury yield briefly reached a 20-year peak. While this has been a drag on bond returns this year, it also means that bond yields are attractive by historical standards. When it comes to generating income in a portfolio, this environment continues to offer meaningful opportunities.

Perhaps most importantly, your financial plan is built to withstand uncertainty around monetary policy. While we do not know exactly how Warsh will govern or how inflation will evolve, history tells us that maintaining a long-term perspective through periods of uncertainty has consistently been the right approach.

I hope this perspective helps as we navigate ever-changing market conditions. As always, please do not hesitate to reach out if you have any questions, or if you would simply like to talk through what any of these developments mean for your specific situation and goals.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

No strategy assures success or protects against loss.